Decoded: Nikhil Kamath Podcast | The Investor Who Doesn’t Predict

Howard Marks on why surviving markets matters more than reading them

Here is the contradiction worth sitting with.

Howard Marks is one of the most cited investors in the world, largely because of his reputation for reading market cycles correctly. And yet in a long conversation with Nikhil Kamath, he spends considerable time arguing that prediction is not the edge. That the investors who survive across multiple market regimes — not just the favorable ones — are organized around a different question entirely.

The contradiction is productive. Because if Marks is right, and the financial press is quoting him for the wrong reason, then most of the people citing him are drawing the wrong conclusion.

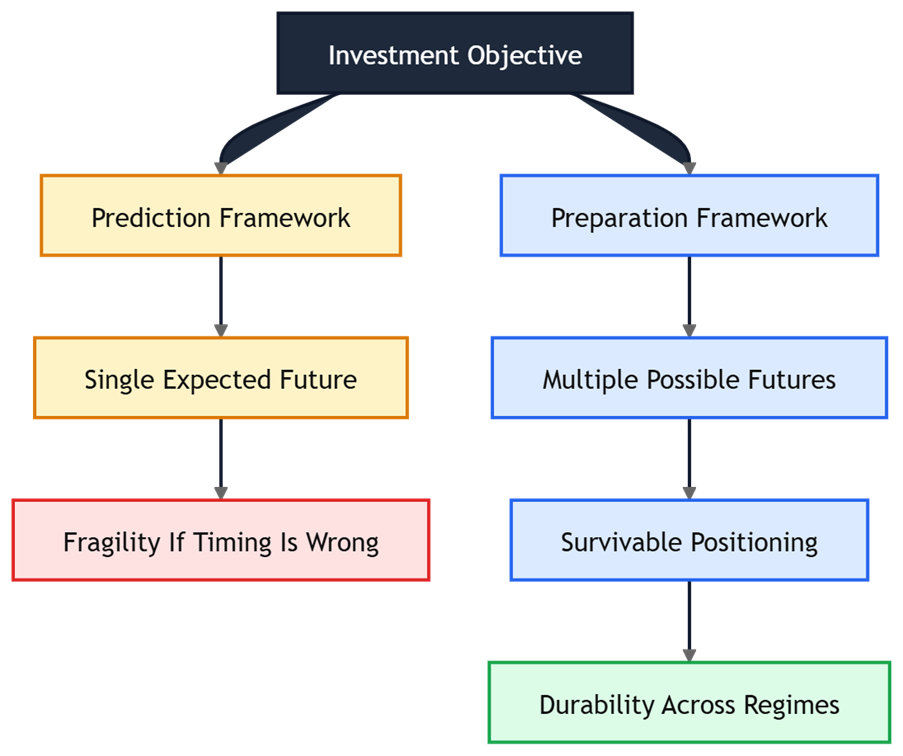

What the prediction frame gets wrong

Most portfolios are built around a single expected future. The investor decides what is most likely to happen, then positions accordingly. This feels like the rational approach. It is how forecasting language works, how research reports are structured, how performance gets evaluated.

The problem is not that forecasting is impossible. It is that forecasting well enough, often enough, under enough pressure to actually build a career on it is a different proposition than it looks. And more importantly, it is the wrong objective.

Marks draws the distinction precisely. An investor who correctly identified the direction of the 2008 housing correction but entered the position 18 months early faced exactly the same redemption pressure as the investor who predicted nothing. The thesis was right. The timing was wrong. The portfolio was closed before it could be vindicated.

Being eventually right and being right in a way that you can survive long enough for it to matter are two different problems. The prediction frame treats them as one.

What preparation actually means

The alternative Marks describes is not passive or passive-adjacent. It is not indexing, and it is not avoiding decisions. It is building a portfolio that produces an acceptable result across a range of futures, including the ones you did not model.

The practical cost of this is a lower expected return in favorable conditions. A preparation-based portfolio does not maximize for the best case. It holds a floor under the cases you didn’t forecast — because some of them will arrive regardless of what the research said.

Diversification is often explained as risk reduction. The deeper explanation is that diversification exists because certainty about future outcomes is unavailable. If any investor had genuine certainty, diversification would be pure cost — money left on the table. The fact that every serious institutional investor diversifies is already an implicit acknowledgment that prediction is insufficient. The behavior just hasn’t caught up to what it actually implies.

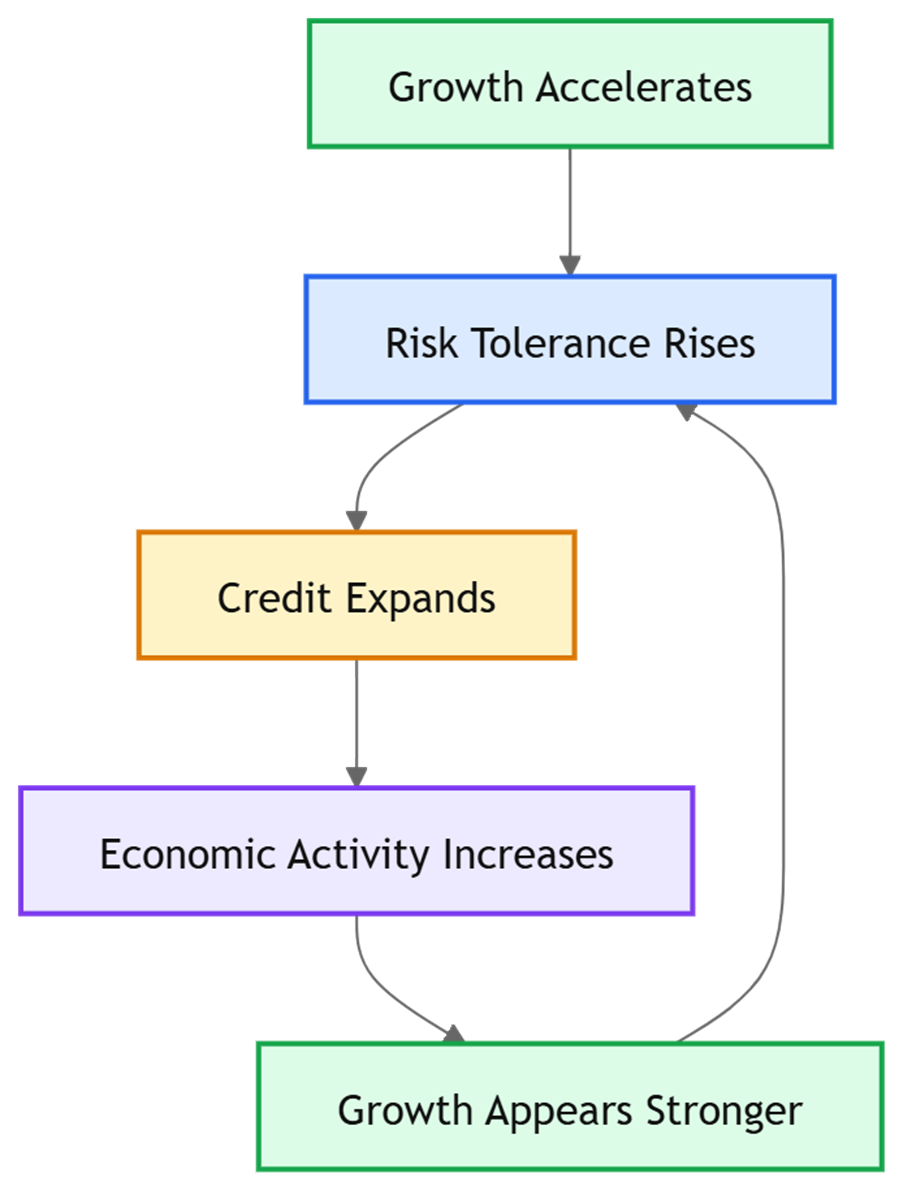

Why cycles persist regardless of information

The natural objection to cycle-based thinking is that better data and faster processing should smooth things out. Cycles should be arbitraged away. More participants, more information, more computing — the inefficiencies narrow.

This hasn’t happened. Not because markets are irrational, but because cycles are not caused by information gaps in the first place.

When growth accelerates, risk tolerance rises. Rising risk tolerance expands credit. Expanded credit funds more activity, which makes growth look better, which raises risk tolerance further. Every actor inside that sequence is making a defensible individual decision. The overshoot is what their aggregated rational behavior produces. No amount of better information changes the human reflex that drives it. Technology changes the speed of cycles. It does not change the architecture.

The correction runs identical logic in reverse, and it always will.

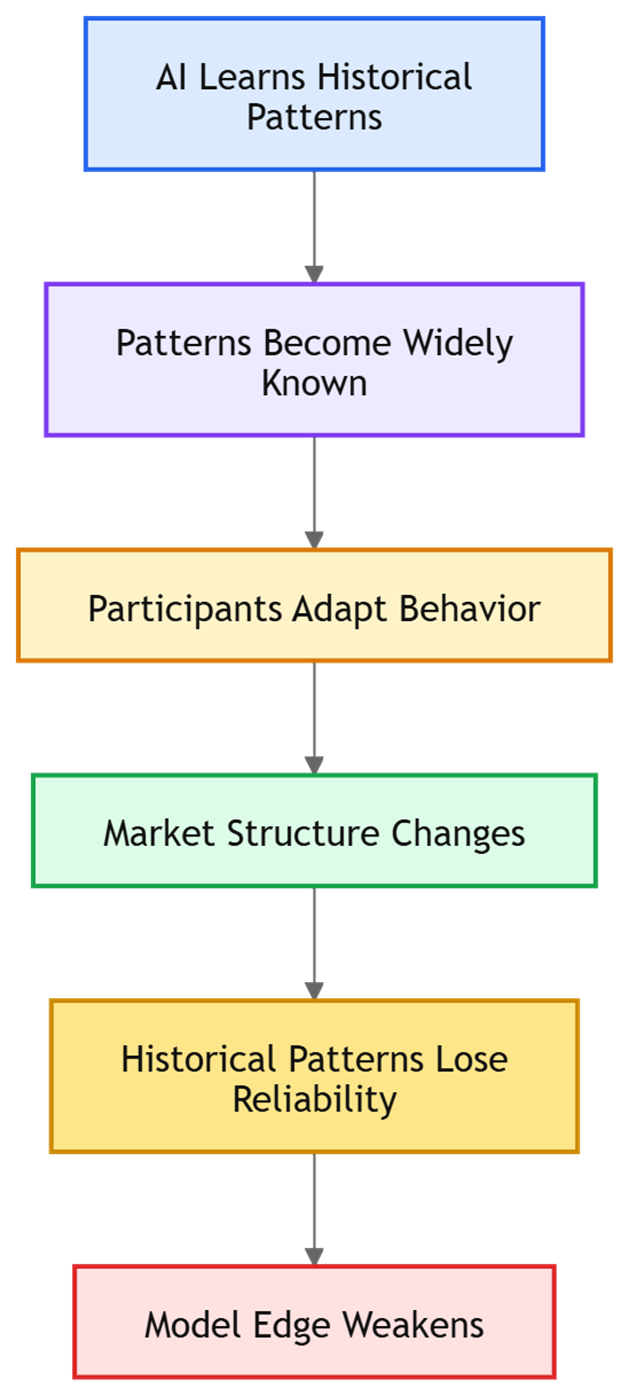

Where AI changes the math — and where it doesn’t

The current argument about AI and investing tends to collapse two different edges into one. Marks separates them.

The first edge is processing publicly available information faster and more completely than competitors. This edge was already compressing before large language models existed. AI accelerates a trend already in motion. If your advantage came from reading more quickly or modeling more variables, that advantage is already being eroded and will continue to be.

The second edge is different. It comes from genuinely different interpretation of available information. From the capacity to hold a position through institutional pressure and social discomfort. From identifying possibilities that have no historical precedent — which means no training data, no pattern recognition, no extrapolation from prior behavior.

Markets are reflexive. Participants adapt to known patterns, which changes the patterns. An AI trained on how a market behaved when a particular pattern was unknown is being applied to a market that has since adjusted to that pattern. The model is chasing something that moved.

Average analytical capacity gets automated. The judgment above that threshold becomes more scarce, which means more valuable, not less.

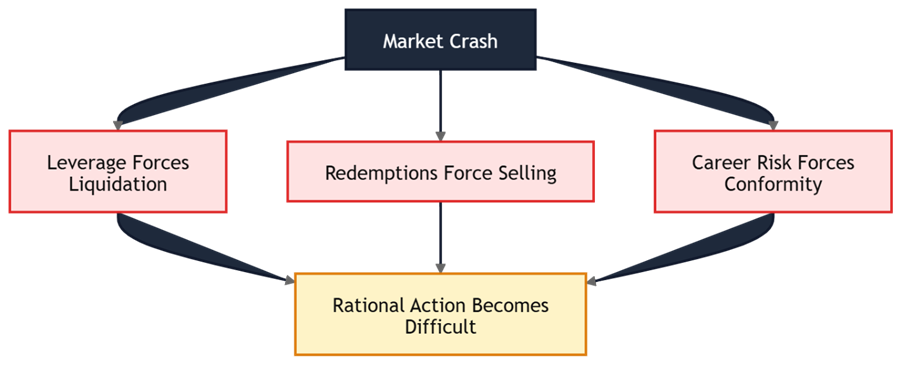

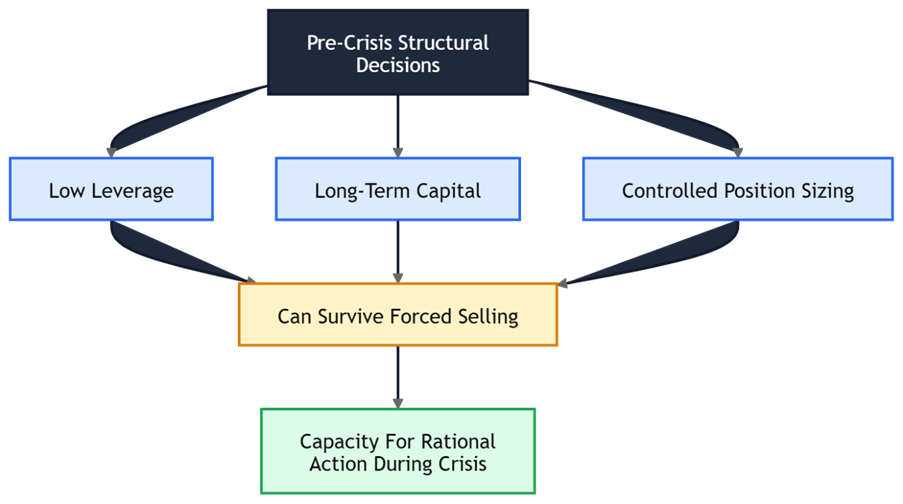

Why emotional control is a structural decision

This is the part of the conversation that lands hardest, and it is the most misread.

The opportunity during a market crash is usually visible. The valuations are there. The thesis is available. Most investors cannot act on it — not because they lack courage or conviction, but because they are operating inside conditions that make rational action genuinely impossible.

Leverage forces liquidation before thesis quality matters. Institutions facing redemptions must raise cash regardless of what they believe about valuations. Career incentives create enormous pressure to demonstrate caution, which means selling what the market is selling, not buying what it is offering. Recent losses distort probability assessment in the direction of more caution precisely when less caution is warranted.

None of this is a character failure. It is a structural outcome.

Which means the capacity to act during a crash is built before the crash. An investor without leverage, whose clients carry long time horizons, who has not recently underperformed a benchmark badly enough to trigger career risk — that investor enters a crisis in a different structural position. The emotional stability that looks like discipline in hindsight is mostly a consequence of decisions made in calmer conditions.

You cannot build the capacity for rational action in a downturn by trying harder in the moment. You build it earlier, when nothing is wrong, when the decisions feel smaller than they are.

What this leaves open

Marks is not describing a better model for predicting markets. He is describing a different objective: survive the futures you didn’t forecast, because some of them will arrive regardless of what you expected.

The uncomfortable implication is that most investment frameworks — most of the research, the reporting, the performance evaluation — are organized around the wrong question. They are asking what will happen. The question that actually produces durable results, across multiple market regimes, through the crashes and the recoveries and the ones nobody modeled, is: what range of outcomes do I need to survive?

That reframe does not make investing simpler. It makes it more honest about what the problem actually is.

Which is, in the end, a more useful kind of difficulty to be working on.

Source

References

Primary Source

Howard Marks: AI, Debt vs Equity & The Next 40 Years Of Investing | Nikhil Kamath | People by WTF

Optional Supporting Reading

Howard Marks Memo Archive (Oaktree Capital)

https://www.oaktreecapital.com/insights/memosThe Most Important Thing by Howard Marks

https://www.oaktreecapital.com/insights/books/the-most-important-thingHoward Marks Memo: The Illusion of Knowledge

https://www.oaktreecapital.com/insights/memos/the-illusion-of-knowledgeHoward Marks Memo: Is It a Bubble?

https://www.oaktreecapital.com/insights/memos/is-it-a-bubble

Comments

Post a Comment